Welcome to Episode 31 of the Preferred Shares Podcast.

In this episode, we continue to focus on Nestlé. We brought back our guest Mark Purdy (whom we interviewed about Lindt & Sprüngli) to chat about the company’s more recent history and its current set of challenges and opportunities. Mark is a veteran investment analyst with 40 years of experience with a particular focus on consumer brands. He’s now retired from full-time research and portfolio management, and he has set up Calabria Park Advisors, a boutique consultancy.

In This Episode

Setting the Stage: Consumer Staples Under Pressure — Mark frames the last six years for the sector, covering the COVID distortion between in-home and out-of-home consumption, and the wave of inflation that followed.

Nestle’s Perfect Storm: Cocoa & Coffee Costs — Commodity prices hit Nestlé especially hard, with cocoa at one point nearly 5x its pre-spike level, squeezing margins.

CEO Carousel: Three Leaders in 18 Months — The show examines the transition from Paul Bulcke to Mark Schneider to Laurent Freixe and now Philippe Navratil, and how leadership instability can create internal distraction even at a resilient company.

The Case for Insider CEOs in Consumer Staples — Mark argues that the long-cycle nature of brand stewardship favors internal promotions, and why Navratil’s 20-year tenure and track record make him a credible candidate.

Brand Portfolio Sprawl — A discussion of how consumer goods giants naturally accumulate thousands of brands despite every CEO promising “fewer, bigger, better,” and what Nestlé should actually do about it.

M&A Winners and Losers: Ralston Purina vs. Health Science — Mark contrasts Nestlé’s successful acquisitions (Purina, the Starbucks licensing deal) against its costly failures in vitamins, wellness, and Jenny Craig, and explains why working capital mismatches can doom category expansions.

The KitKat Exception and Confectionery Regrets — Despite owning iconic Rowntree’s brands, Nestlé largely squandered its confectionery position — with KitKat the lone standout — while watching Lindt thrive on its doorstep.

Capital Allocation Priorities: Dividends, Debt, and RIG — Mark digs into Nestlé’s current financial constraints, a stretched ~70% dividend payout ratio, rising net debt, and why CEO Navratil’s new focus on Real Internal Growth (RIG) — a metric Nestlé itself invented — is the only viable path forward.

The L’Oreal Stake: Financial Asset or Get-Out-of-Jail Card? — Mark walks through the 50-year history of Nestlé’s ~20% stake in L’Oreal and the logic (and politics) of gradually selling it down.

Closing Advice to the Board — Mark’s prescription: Nestlé must recognize its genuine strengths (emerging market reach, scale, R&D); stop chasing growth through ill-fitting acquisitions; and be patient. A steady 3% real sales growth rate has historically been more than enough to create a very attractive shareholder return.

Charts and Images

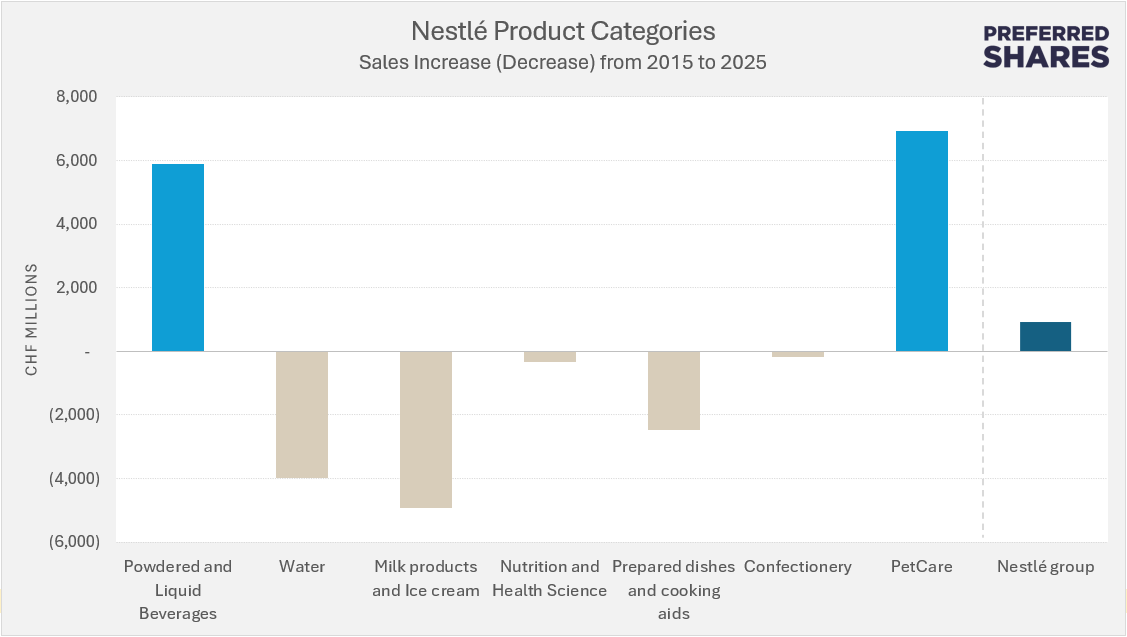

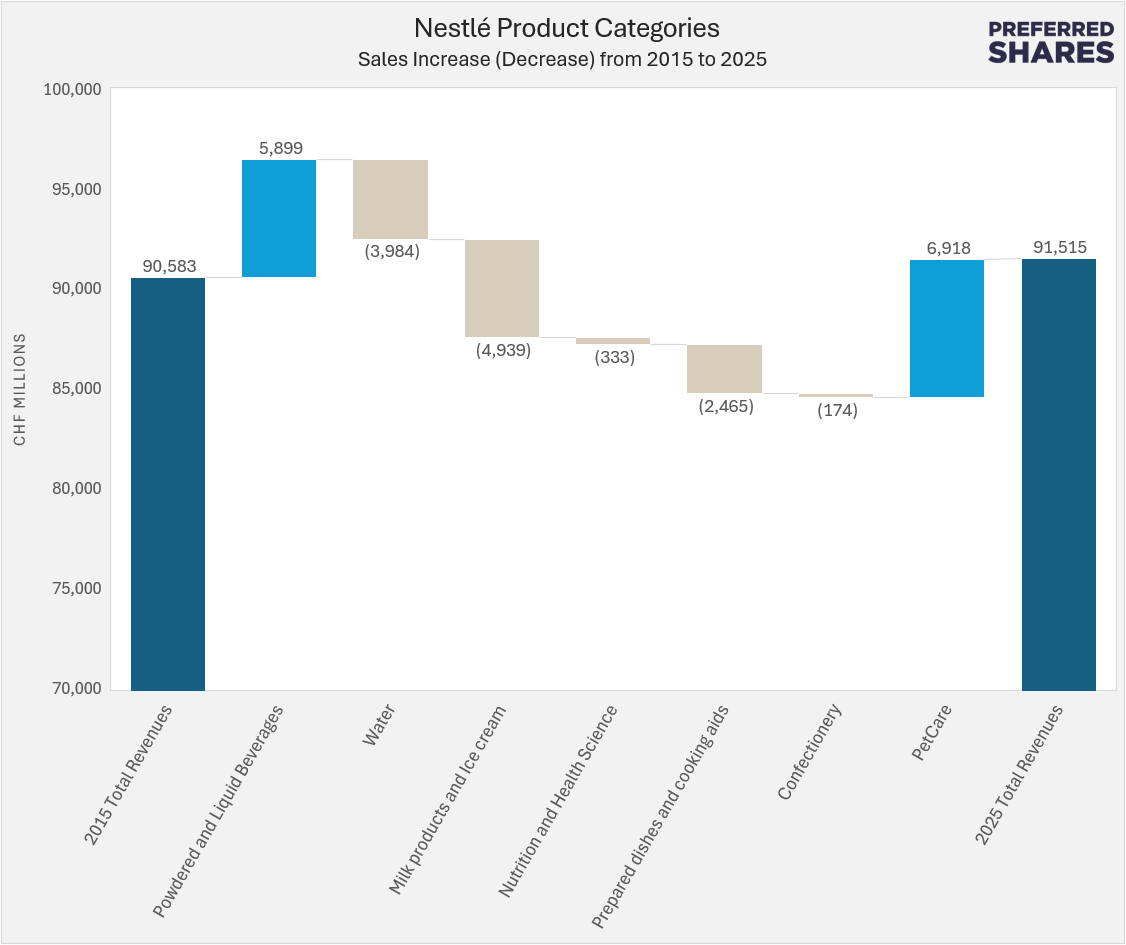

The two charts below show the total increase decrease of Nestlé’s seven product categories over the last ten years. The two growth categories have been Powdered and Liquid Beverages and PetCare, while the others have been down or flat. The result has been total sales not increasing by much for Nestlé over the prior decade.

Click on the graphic below for a great article published on Oct. 24, 2018, by The New York Times, about the amazing popularity and variety of Kit Kats in Japan.

Additional Reading & Listening

Did you miss our episode on the early history of Nestlé? Just click the link below!

Curious to see what else we’ve been working on? Check out some of the interesting things we’ve done recently:

Douglas Ott (Andvari Associates and @yesandnotyes)

Lawrence Hamtil (Fortune Financial and @lhamtil)

Devin LaSarre (Invariant and @DevinLaSarre)

Enjoy this episode? Share it with someone who loves business history as much as you do!

You can also follow Preferred Shares, Devin, Doug, and Lawrence on Twitter.

Disclaimer

All opinions expressed by Preferred Shares hosts and guests are solely their own opinions and do not reflect the opinions of their respective employers. This podcast is for informational and entertainment purposes only and should not be relied upon as a basis for investment decisions. None of the information contained in the podcast or this web site constitutes a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person.

Clients of Andvari and Fortune Financial may maintain positions in the securities discussed in this podcast. Furthermore, from time to time, the Hosts may hold positions or other interests in securities mentioned in the Podcast and may trade for their own accounts based on the information presented. At the time of publishing, clients of Andvari and Fortune Financial owned shares of Nestle. The Hosts may also take positions inconsistent with the views expressed in its messages on the Podcast.